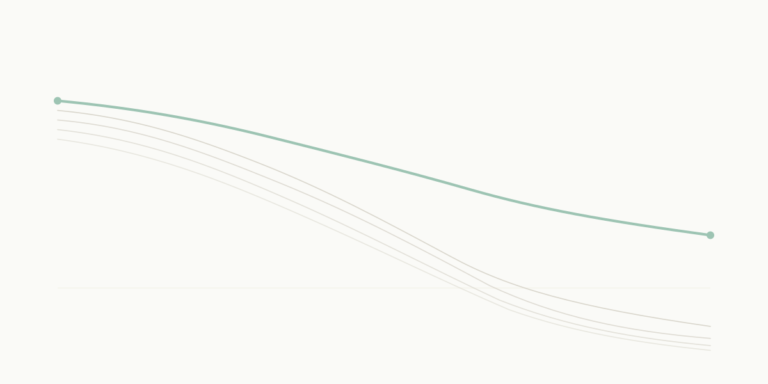

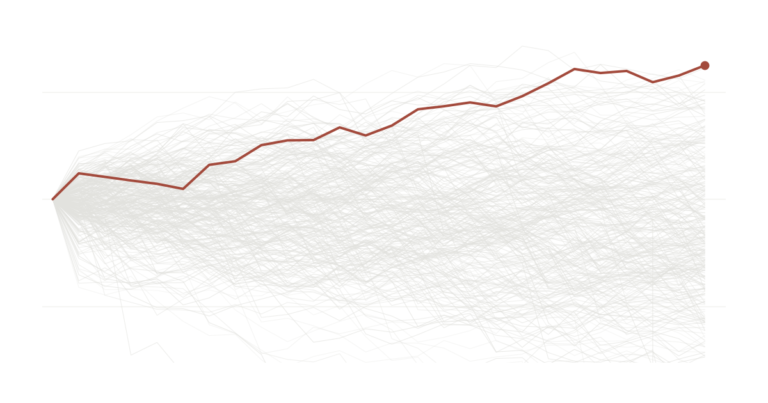

The advice you’re getting may not be replicable

Thousands of Indian investors borrowed early, concentrated hard and held through the falls. You have only ever heard from the ones it worked for. A look at why the origin stories of famous investors are poor instructions, and the three questions to ask before copying any of them.