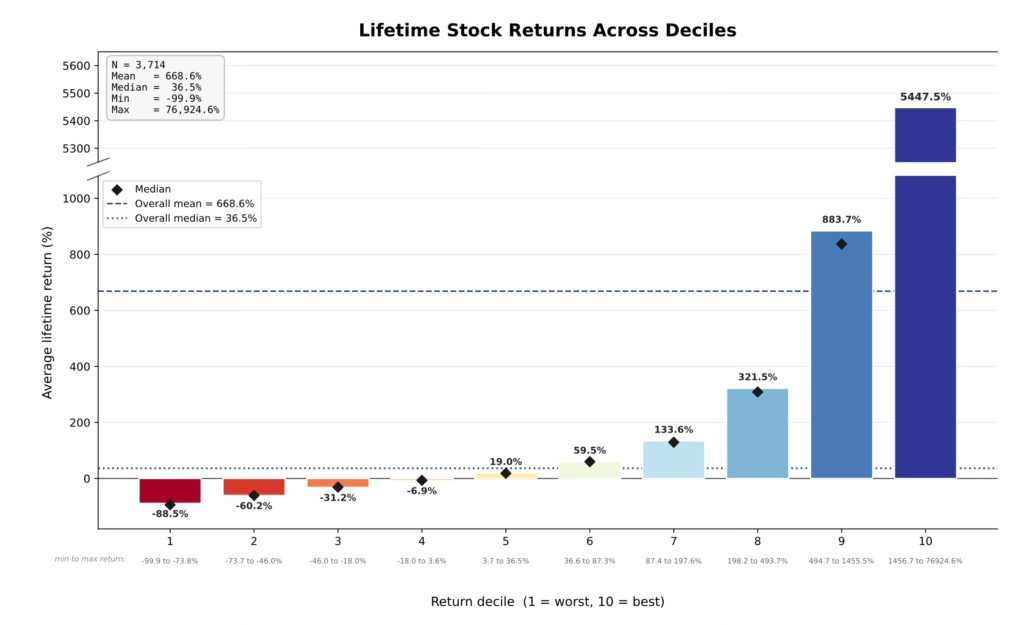

Hendrik Bessembinder asked a deceptively simple question of US stocks: do they actually beat Treasury bills? The answer, for most of them, was no. We ran the same test on the Indian market with an equal weight assigned to each of the stocks i.e. “an equal bet in every stock”, 3,714 NSE stocks, 2005 to 2026, each held from its listing to its exit, measured against a liquid fund earning around 6%.

From the research, nearly half the universe, 49.7%, failed to beat that 6% bill. More than a third of the listings (~38%) lost money outright. The median stock returned nearly 37% over its entire life, which, spread across a median holding of close to eight years, barely clears the risk free rate while carrying every ounce of single-stock risk. Then the average stock returned nearly 669%.

The Gap Is the Whole Story

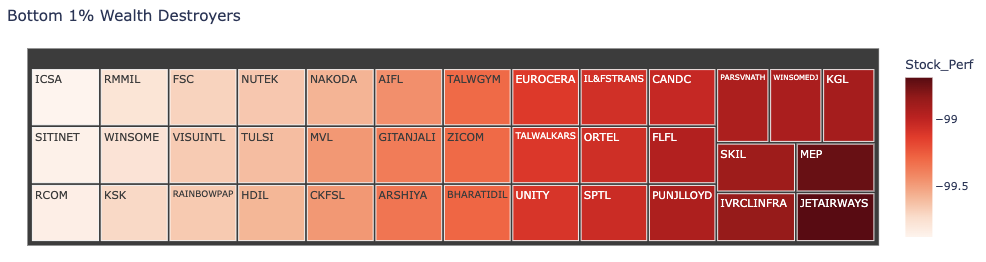

That gap is the whole story. Mean 669%, median 37%. The average stock is eighteen times the typical stock, because a small group of names is doing genuinely absurd things. BAJFINANCE compounded to +76,924%. Meanwhile the bottom decile sits in a graveyard around -90%, with several names (ICSA, RMMIL, KSK) riding all the way down to -99%.

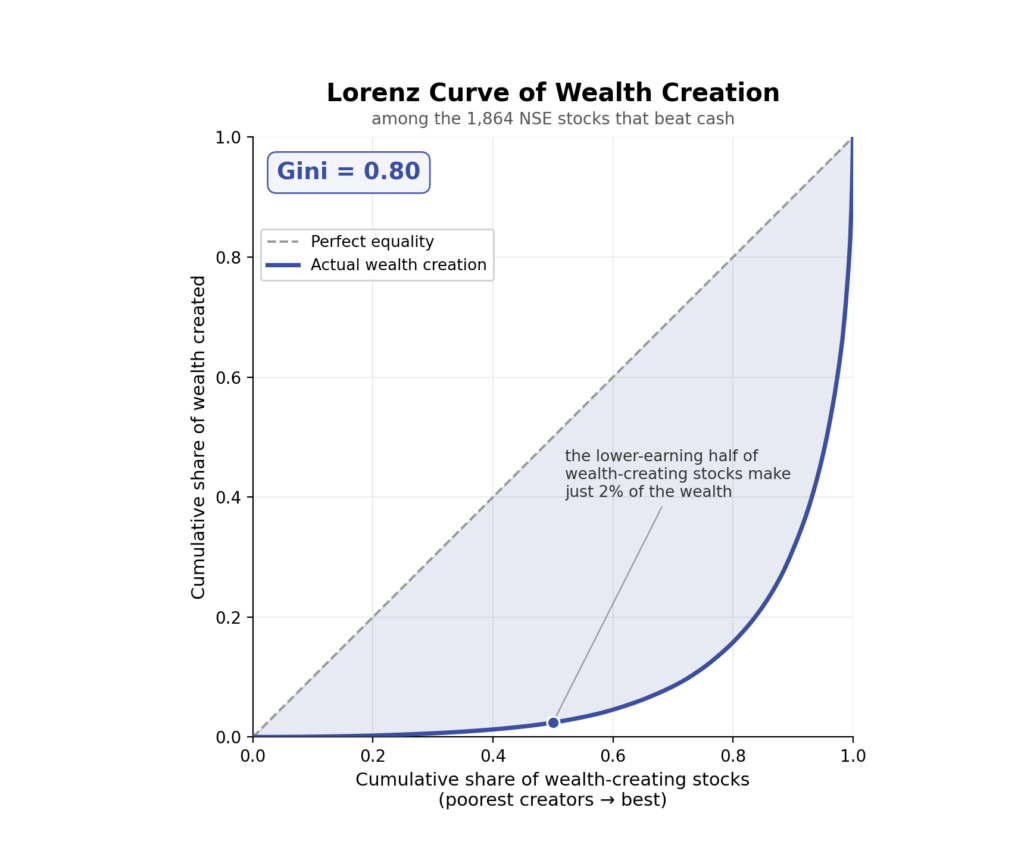

A Handful of Stocks Make Almost Everything

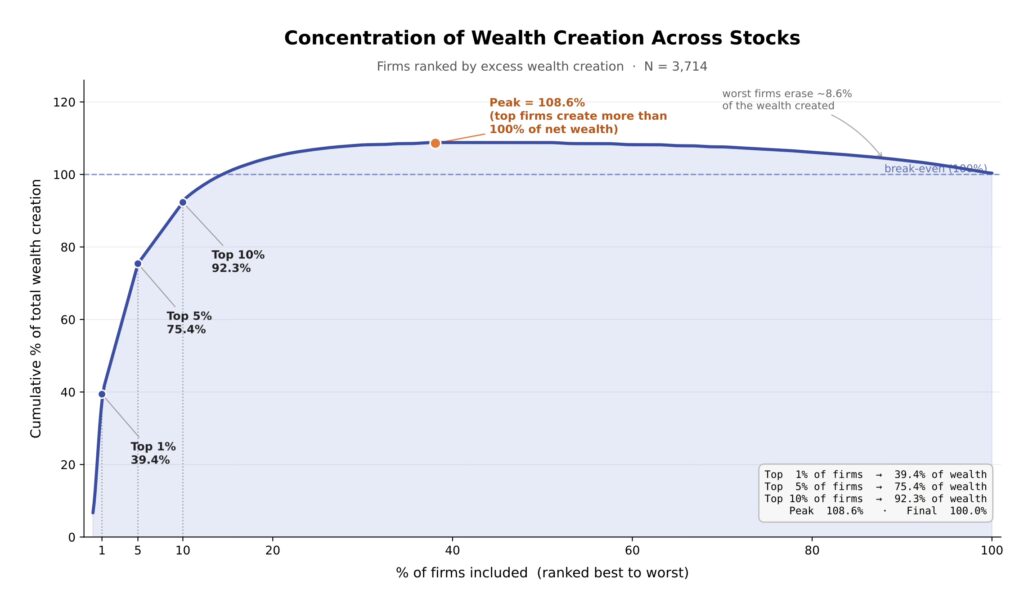

Stack the winners up and the concentration is brutal. The top 1% of stocks created nearly 40% of all the net wealth. The top 5% created about three quarters of it. The top 10% created nearly 92%. The entire bottom 90%, combined, produced the remaining 8%. Also important to note, the wealth curve climbs past 100% before sagging back down to it, the losing names are not merely unproductive, they actively destroy nearly 8% of the wealth the winners built.

Push the ranking out a little further and the verdict gets starker. Only about the top 15% of names ever create any lasting net wealth at all. Everything past that, taken together, nets to nothing, because the dead weight in the basement cancels out the modest winners in the middle. Scoring the top decile winners against the rest of the winners lands the Gini coefficient near 0.80, a level of concentration no real economy ever reaches.

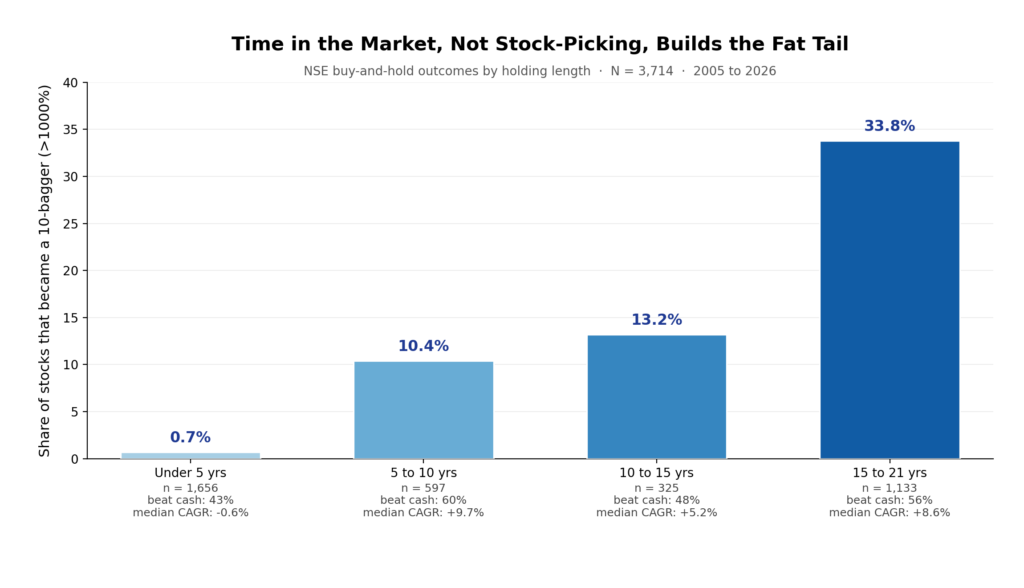

The Big Winners Are Built by Time

We also need to ask, where do those few enormous winners actually come from? Almost entirely from time. Sort the universe by how long each name was held and the pattern is impossible to miss. Among stocks with less than five years of listing, fewer than one in a hundred ever became a ten bagger, posting a median negative return. Although there is a recency bias in there as nearly 40% of our stock universe is of companies listed after 2021. Among stocks held for fifteen to twenty one years, a full third of them crossed ten bagger territory.

The median big winner took close to two decades to get there. No single explosive tick. A long, patient climb. Annualise the whole universe and the median name compounds at about 5.8% a year against the liquid fund’s 6%. So the middle of the market does not even clear the bar it is measured against.

This matters more than it first looks. The fat tail is built by duration, which means selling a real winner early is how we quietly wreck our own returns. But it also exposes the flaw in the comfortable version of buy and hold. Time only pays us if we are sitting in the right names, and half the market spends those very same years bleeding toward the basement.

“Just Buy the Market” Is Only Half the Answer

So the popular conclusion is “just buy the market,” and that is half right. Owning everything guarantees we own the winners like AVANTIFEED, at the price of also owning every -99%. Brute force works precisely because it never has to guess.

The hard problem is identifying the 4 to 15% of names that actually matter, and we cannot know them in advance. This is where trend following earns its seat at the table. It does not try to forecast the winners. It lets price reveal them, stays with revealed strength, and exits revealed weakness long before a stock reaches the -99% basement.

The shape of the curve is the point. A trend-following payoff is convex, a stream of many small losses paid for by a few enormous wins. That is the mirror image of the return distribution above. We are matching the shape of our strategy to the shape of the opportunity, landing us a higher compounded return than holding everything blindly.

The Two Honest Ways Out

The key takeaway for now is narrower, and more useful, than “buy and hold is dead.” It is this – buying one stock and never selling is the losing game. Owning everything, or systematically following strength, are the two honest ways out.

References

Bessembinder, Hendrik (Hank), Do Stocks Outperform Treasury Bills? (May 28, 2018). Journal of Financial Economics(JFE), Forthcoming. Available at SSRN: https://ssrn.com/abstract=2900447 or http://dx.doi.org/10.2139/ssrn.2900447

Bessembinder, Hendrik (Hank), One Hundred Years in the U.S. Stock Markets (March 18, 2026). Available at SSRN: https://ssrn.com/abstract=6438198 or http://dx.doi.org/10.2139/ssrn.6438198