In 1952, a 25-year-old PhD student at the University of Chicago published a paper that changed how the world thinks about investing. Harry Markowitz proposed that an investor should not just maximise return, but maximise return per unit of risk. He defined risk as standard deviation. The volatility of a portfolio’s returns. How much it bounces around its mean.

The paper won him a Nobel Prize. It also created the framework that every financial advisor, every CFA candidate, every wealth manager learns first. Risk-adjusted returns. The Sharpe ratio. The efficient frontier.

The framework is mathematically elegant. It is also wrong for most of the people it gets applied to.

What the math actually says

Take two investors with twenty-year horizons.

Investor A finds an asset that compounds at 12% annually with low volatility. Smooth ride. Barely a bad year. Sleeps well.

Investor B finds an asset that compounds at 20% annually with high volatility. The portfolio drops 30% one year, jumps 50% the next, falls 40% three years later. Sleeps poorly.

Modern Portfolio Theory says Investor B is taking on more risk. The Sharpe ratio prefers Investor A. Most financial advisors will steer their clients towards strategies that look like A and away from strategies that look like B.

Run the math.

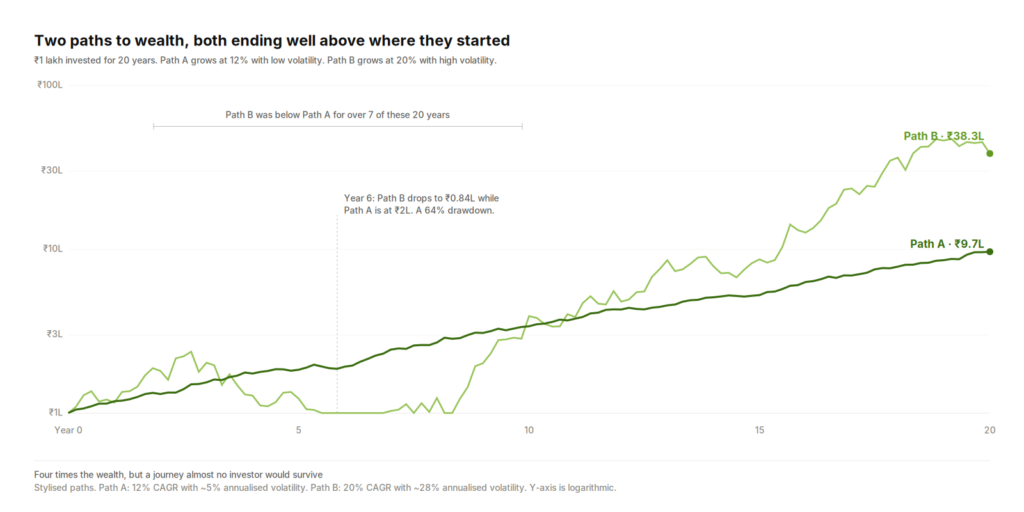

₹1 lakh at 12% for 20 years becomes ₹9.6 lakhs.

₹1 lakh at 20% for 20 years becomes ₹38.3 lakhs.

The gap is ₹28.7 lakhs. Not a rounding error. Not a marginal improvement. Four times the wealth.

The investor who chose A on the advice of risk-adjusted return frameworks ended up with about a quarter of what the investor who chose B ended up with. Both arrived. Only one arrived rich.

Why volatility feels like risk

The answer to why so many people choose A is not that the math is unclear. The answer is that the journey is hard.

Look at Path B in the chart. For more than seven of those twenty years, Path B was worth less than Path A. There was a 64% drawdown along the way. At the worst of it, year 6, the volatile investor was sitting on ₹0.84 lakhs while their friend running Path A had grown ₹2 lakhs. The investor watching their portfolio shrink by 64% does not see a temporary deviation from the mean. They see a permanent loss of two-thirds of their savings. Their brain registers it the way the brain registers any large loss. Loss aversion is real. Behavioural finance has documented it for fifty years.

The drawdown is not where most investors quit. The longer test is the years when nothing seems to be happening. When Path B has been below Path A for two, three, five years in a row. When the steady-handed friend with the index fund is doing better and saying so at dinner parties. That is when the volatile investor sells.

So the standard advice has a kernel of truth inside it. For an investor who will not survive Path B, the volatility is not theoretical. It is the thing that ends the experiment early. A 35-year-old who picks Path B and sells in year 7 has not earned 20%. They have earned the worst possible compounding of bad timing. The honest finding is that the volatile path delivers the higher return only to the investor who actually holds it for the full twenty years. Which is a smaller group than the one that promises themselves they will.

Where the framework breaks

The Modern Portfolio Theory framework was designed in the 1950s for people who needed to draw down their portfolios on a fixed schedule. Pension funds. Insurance companies. Endowments with known annual obligations. For an entity that needs to liquidate ₹X in eighteen months, volatility is risk. A 30% drawdown three months before the obligation is real damage.

The framework gets misapplied when it is handed unchanged to a 35-year-old whose only forced sale is twenty years away. For that investor, the volatility between now and year 18 has no consequence as long as they do not sell. Their actual risk is something else entirely.

Their actual risk is path-dependent loss. Selling at the wrong moment. Failing to compound for long enough. Reaching retirement with a portfolio that grew at 6% when it could have grown at 15%. The shortfall against what was needed.

By that definition, the safest portfolio for a 30-year-old is the one that produces the highest long-run return that the investor can actually hold without selling. Volatility only matters as a constraint on holding power. Not as a measure of risk in itself.

The age-based reframe

This suggests a simple framework that the textbooks should have written and never did.

Under 45. Chase absolute returns. Volatility is irrelevant. The compounding window is too long for short-term price action to matter. The investor’s job is to find the highest-returning strategy they can actually hold without panic-selling. Diversification still matters. Position sizing still matters. But Sharpe ratios should not drive the asset allocation.

45 to 60. Volatility starts to count. The compounding window is shrinking. A bad sequence of returns close to retirement can permanently impair the outcome. This is when risk-adjusted returns become useful, not before.

Over 60. Risk-adjusted returns become the right framework. Now the investor is liquidating regularly. Volatility is real risk. The 60-year-old who is drawing 4% of their portfolio every year cannot afford a 50% drawdown without permanent damage to their lifestyle.

The textbooks teach the third framework to the first audience. They tell 30-year-olds to optimise for Sharpe ratio when they should be optimising for terminal wealth. The cost of that misapplication is not abstract. It is roughly ₹29 lakhs over twenty years, on a starting capital of ₹1 lakh. Scale that to a real portfolio and the gap runs into crores.

The non-negotiable rule

There is one place where the contrarian view collapses. One rule that overrides everything written above.

Your portfolio cannot blow up. Ever.

Volatility is not risk. Permanent capital impairment is risk. The two get confused because they both make a portfolio go down, but they are completely different events. A 64% drawdown that recovers is volatility. A 100% loss that does not recover is ruin.

The investor chasing Path B in the chart above must rule out, with certainty, the possibility of a permanent zero. That means no leverage that can margin-call them out at the worst time. No single concentrated bet that can go to zero. No untested derivative strategy with hidden tail risk. No instruments that can fail in ways the investor does not understand.

Volatility is acceptable because it eventually mean-reverts. Ruin is not, because there is nothing on the other side of zero. An investor in their thirties can survive a 64% drawdown. They cannot survive a 100% drawdown. The fund manager who blew up in 1998 with a Sharpe ratio of 4.0 is not coming back to compound for another decade.

The rule is not “take maximum volatility.” The rule is “take as much volatility as the investor can hold, in instruments that cannot zero out.” Those are different rules and both have to be obeyed.

What this means in practice

Most retail investors in India have been told that Nifty 50 ETFs and large-cap funds are “safe.” They are. They are also a poor fit for someone with a twenty-year compounding horizon. The Nifty 50 has compounded at roughly 12% over the long run. Indian smallcap and midcap indices have compounded at higher rates, with much more volatility, but with similar terminal-wealth advantages over very long holding periods.

The investor who allocated 100% to Nifty 50 because their advisor framed it as “lower risk” did not actually take less risk. They took a different kind of risk. The risk of being underexposed to the highest-compounding parts of the equity market during the only compounding window they have. By the time they are 60, the gap between what they have and what they could have had is permanent.

This is not an argument for taking on every volatile bet. It is an argument for making sure the volatility budget actually gets spent. A 30-year-old running a portfolio with 8% expected volatility is not being conservative. They are being mismatched to their own time horizon.

The most dangerous risk in personal finance is not a 64% drawdown in a decade where the investor has twenty years of compounding ahead. It is following retirement-investing rules when retirement is two decades away. It is treating the framework that protects a 60-year-old’s spending as the framework that should govern a 35-year-old’s saving.

The framework was right. The audience was wrong.

Path A and Path B are stylised illustrations of long-run compounding under different volatility assumptions. They are not specific assets or strategies. The 12% and 20% CAGR figures are intentionally idealised to isolate the effect of volatility on terminal wealth.