A wealth manager said on a podcast last week that you need ₹40 crore to retire comfortably in an Indian metro by 60. One camp called the number outrageous. The other defended it with inflation, healthcare, lifestyle. Both were arguing about arithmetic.

I’m not here to talk about the math. Money isn’t a spreadsheet problem.

The figure quietly assumes everyone reading it is the same person. Same city, same lifestyle, same definition of comfortable, same thirty years ahead. It isn’t an answer. It’s one specific life dressed up as a universal one. It also lives inside a bubble. This is a conversation only a small slice of Indians get to have. If you’re in that slice, the question worth asking isn’t whether ₹40 crore is right. It’s why we always rush to a number, and what we’re missing when we do.

I’ve chased the number. It’s empty when you catch it.

I’d set a corpus target in my twenties. Distant enough to be motivating, close enough to feel real. When I hit it a few years later, I expected something. A pause or a sense of having arrived.

What I felt was a quiet anticlimax, and within weeks I’d raised the target. The new number felt necessary the moment the old one was achieved.

The number was load-bearing because it was distant. Once it became reality, it couldn’t carry the weight of meaning I’d assigned it. What I’d actually wanted wasn’t financial. The number was a proxy for it, and a poor one.

This is the part of the retirement conversation nobody has. People who hit the number and stop are rare. Most raise it. Some can’t stop at all. One more year of cushion. Then another. If you can’t stop at the figure, the figure was never the real issue.

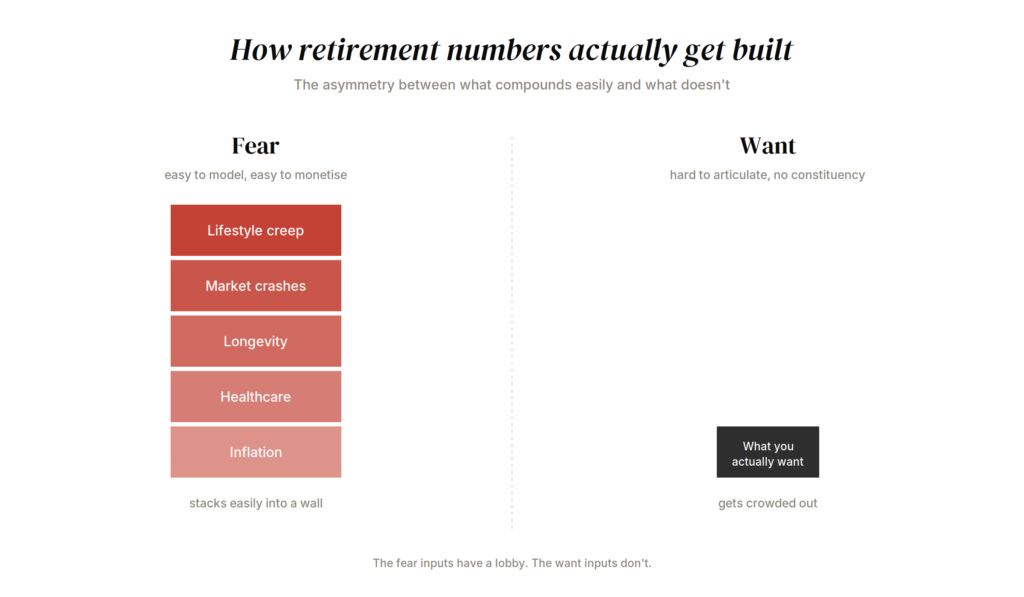

Fear has a lobby. Want doesn’t.

Every large retirement number is built on the fear side of the ledger. Inflation. Healthcare. Longevity. Market crashes. Lifestyle creep. Each compounds easily into something that looks like a wall.

The ‘want’ side, what you actually want your life to feel like, is quieter and harder to articulate. It doesn’t show up on a calculator. It requires sitting with yourself and answering questions most people never ask. So it gets crowded out.

This is why retirement numbers only ever inflate. The fear inputs have a lobby. They’re easy to model, easy to scare people with, and easy to monetise as a service. The want inputs have no constituency. The result is a planning conversation populated almost entirely by defensive variables. You end up building a fortress to protect a life you never paused to design.

The corpus is downstream of choices you already made

And the fortress, once you look closely, is mostly built from materials you ordered yourself.

The number is large because the run-rate became large. The run-rate became large through twenty years of small upgrades, each of which felt rational in the moment. None of them were chosen as a retirement decision. Cumulatively, they set the corpus.

By the time you sit down to plan retirement at 45, the figure feels external, imposed by inflation and the cost of living. It isn’t. It’s the cumulative shadow of your own lifestyle, projected forward.

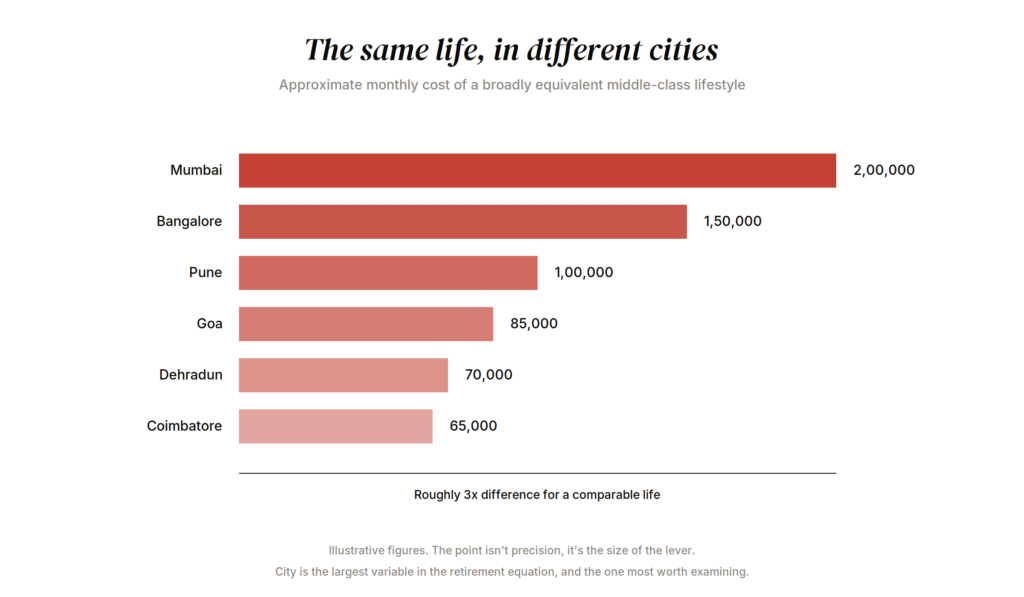

The most uncomfortable variable in the equation is the one almost nobody examines. The same life in Coimbatore, Dehradun, Goa, or Bhubaneswar costs a third of what it costs in Mumbai. People treat their city as a fixed input. It’s the single largest lever in the equation, and the one most worth questioning honestly.

The number assumes a life that doesn’t exist

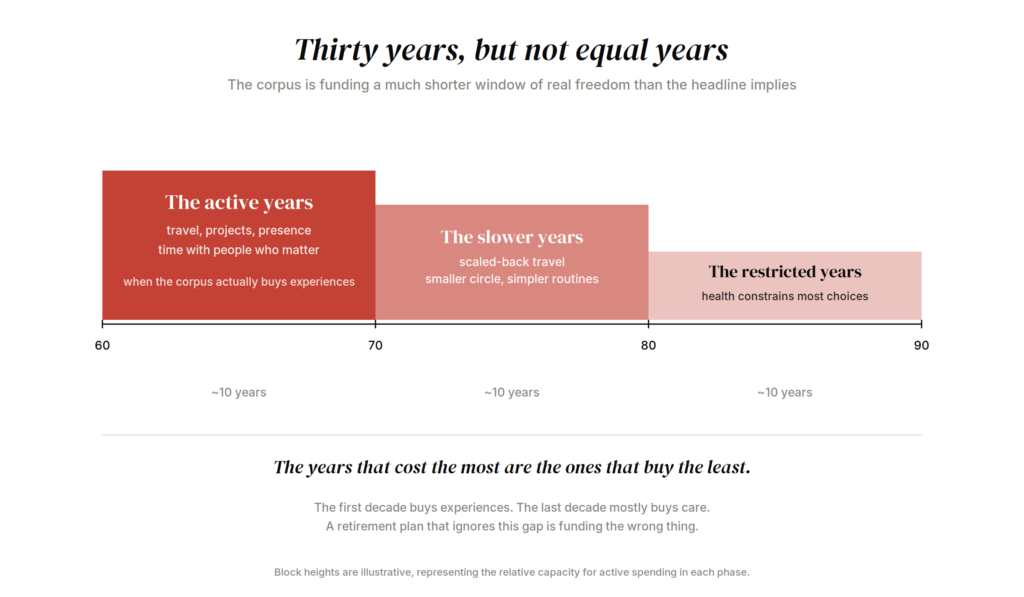

Every large retirement number is built on a quiet assumption that no one tests. That you’ll spend at 80 what you spend at 60, adjusted for inflation. That your run-rate stays flat or rises across thirty years.

The data says otherwise. A long-running RAND study found real spending declines about 2% per year after 65, across wealth groups. A JP Morgan analysis found average spending drops by more than 30% between 60 and 85. These aren’t fringe findings. They come from longitudinal data tracking actual households over decades.

The pattern is consistent and intuitive once you stop assuming. People in their 70s travel less than they did in their 60s. They eat at home more. They stop replacing cars. Their wardrobes don’t refresh. Their social circles narrow. None of this is sad. It’s the natural shape of a life. But every retirement corpus calculation assumes it doesn’t happen, that an 82-year-old needs the same lifestyle budget as a 62-year-old in real terms.

This single assumption is doing more work in inflating retirement targets than any other. Strip it out and most numbers fall by a quarter or more. The ₹40 crore figure isn’t conservative. It’s modelling a person who doesn’t exist.

Time is what you’re actually buying

Strip the corpus question down to its core and what you’re really buying is time. Unstructured time, with the people you want to be around, doing the things that mean something to you. The money is a proxy. The actual asset is the time.

Most people optimise the proxy and never audit the asset. They arrive at 60 with the corpus and discover they have no idea what to do with the freedom. The friends they meant to keep up with are distant. The hobbies they meant to develop don’t exist. The books they meant to read still sit on shelves. The corpus is intact. The capacity to enjoy what it bought has atrophied.

A useful exercise. Forget the postcard version of retirement: the beach and the white hair and the grandchildren. Picture an ordinary Tuesday afternoon at 67. Where do you wake up? Who’s around? What fills the day? What’s on the table at lunch? What’s the conversation in the evening? If the picture is blank, no corpus solves the problem. If the picture is clear, the corpus you need usually shrinks.

What money is actually for

The corpus question, asked properly, isn’t how much do I need. It’s how much do I need so that the gap between what I have to do and what I want to do is as wide as possible, for as long as possible.

That gap is what money is for. It’s the only thing money does that nothing else can do. The figure that funds it for you, given your life, your city, your work, your people, your idea of a good Tuesday afternoon, is your number. It might be ₹40 crore. It might be ₹6 crore. It might be a paid-off home, a modest portfolio, and a slower city. All three can be correct.

The work isn’t to find a better number. It’s to find the picture the number is supposed to fund. Until you have the picture, no figure will feel like enough, and every figure you hit will feel like the wrong one.

The wealthiest people I know aren’t trying to escape their lives. Their retirements look almost identical to the lives they were already living, minus the parts they hated.

The most expensive retirement is the one built to impress people you don’t know, in a city you don’t need to live in, funding a life you never paused to choose.

References

- Hurd, M. and Rohwedder, S. Spending Trajectories After Age 65: Variation by Initial Wealth. RAND Corporation, 2022. rand.org/pubs/research_reports/RRA2355-1.html

- J.P. Morgan Asset Management: Retirement by the Numbers.

Some of the thinking in this piece was shaped by Morgan Housel’s How to Spend Money. If anything here landed, the book is worth your time.