Data-backed writing on markets and money. Zoom Out to see the big picture.

Stay zoomed out. One email a week.

Latest

-

The velocity ceiling: why an Indian melt-up won’t look like Taiwan’s

The Nifty cannot melt up the way Taiwan’s market just did, and the reason is the same thing that keeps it from blowing up.

-

News & Noise

A short game about trading the news. 12 real headlines, 12 real market reactions, your portfolio on every call. Takes about 8 minutes.

-

The Legibility Trap

Why retail investors fixate on fees and taxes, and miss what actually moves their returns

-

Momentum doesn’t fall like high-flyers

The thinking says high-flying stocks crack first in a correction. The latest fall in Indian equities says otherwise. The 240 NSE stocks that had run up the most going in had a median return of around −9.5%, almost four points shallower…

-

Why Being Right 60% of the Time and 40% of the Time Can Both Make You Rich

One of the most common questions investors ask is, “what percentage of your trades are winners?” It sounds perfectly reasonable. And honestly, it’s the same question I would have asked a few years ago. We’re wired to think in terms of…

-

Volatility is not risk. It only feels like risk

Modern Portfolio Theory taught a generation of investors that risk equals volatility. That conflation is fine for a 60-year-old living off their portfolio. For a 30-year-old with three decades of compounding ahead, it is one of the most expensive ideas in…

-

Why every retirement number is wrong

Money is not a spreadsheet problem. The conversation keeps pretending it is.

-

The factor that won, and what it cost

Most equity investors think they own “the market.” They actually own a factor. Over 21 years on Nifty 500 data, the gap between the best and worst factor turned ₹1 lakh into either ₹52 lakhs or ₹13 lakhs. The interesting part…

-

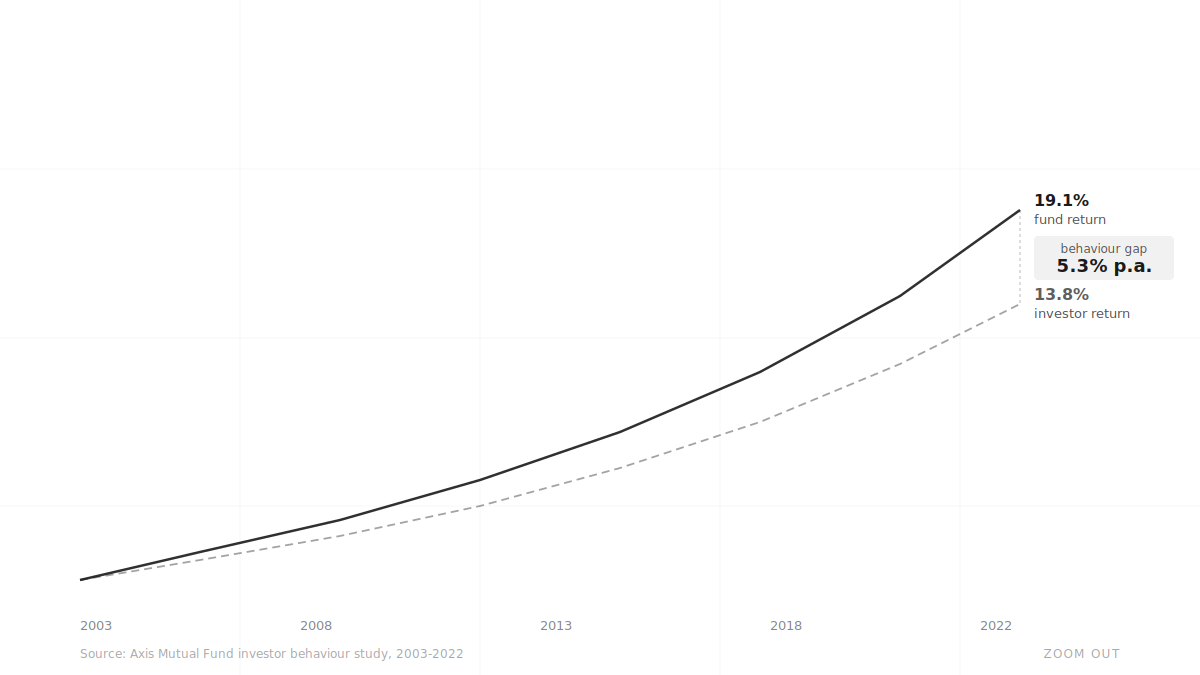

Why retail investors keep buying tops and selling bottoms

Equity funds delivered 19% CAGR over 20 years. The average investor in those same funds earned 14%. That 5 percentage point gap is not a fees problem. It is not a fund selection problem. It is a behaviour problem — and…

-

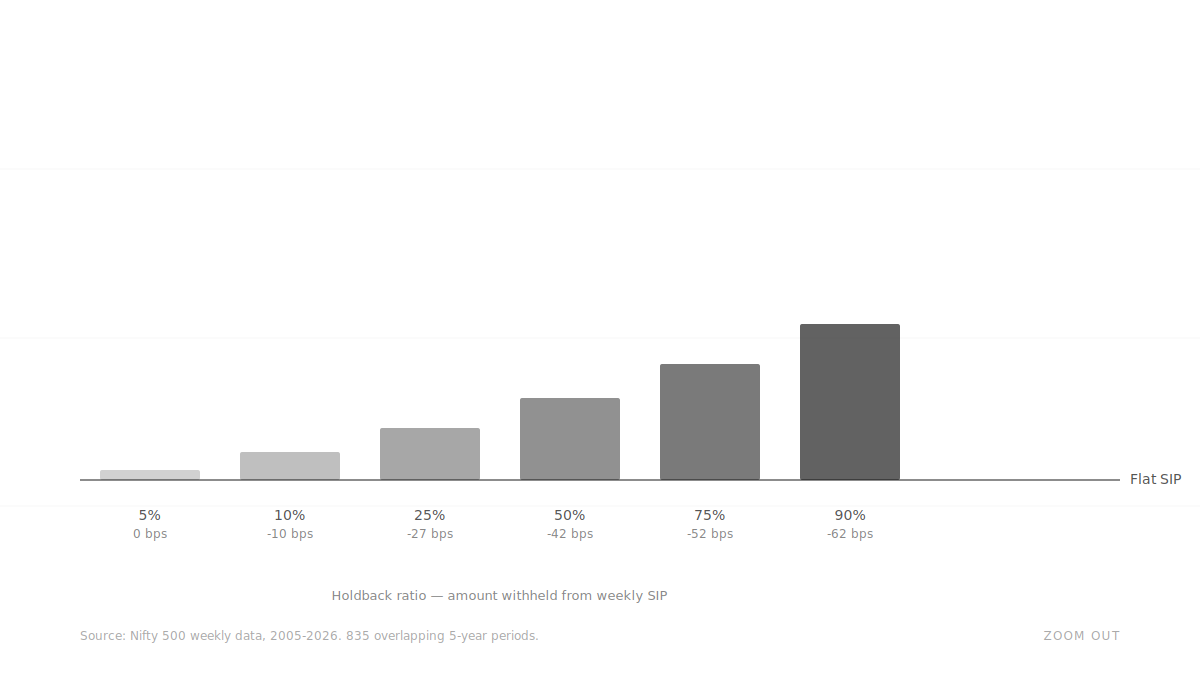

“Buy More When Markets Fall” – Does It Actually Work?

We tested 835 overlapping 5-year periods on Nifty 500 data. At every holdback ratio, the Buy the Dip SIP loses to a flat SIP. The more you hold back, the more you lose. The dumb SIP wins because it never hesitates.